In Australia, a country that prides itself on innovation and entrepreneurship, startups face a daunting challenge: securing bank funding. This conundrum is not unique to Australia but is amplified by local economic and regulatory factors, creating a complex environment for budding businesses. Despite the nation's robust economy and supportive startup ecosystem, why do banks shy away from funding these early-stage ventures? This article delves into the heart of this issue, offering insights backed by data, expert opinions, and real-world case studies, while challenging common misconceptions about startup financing.

The Australian Startup Landscape: An Overview

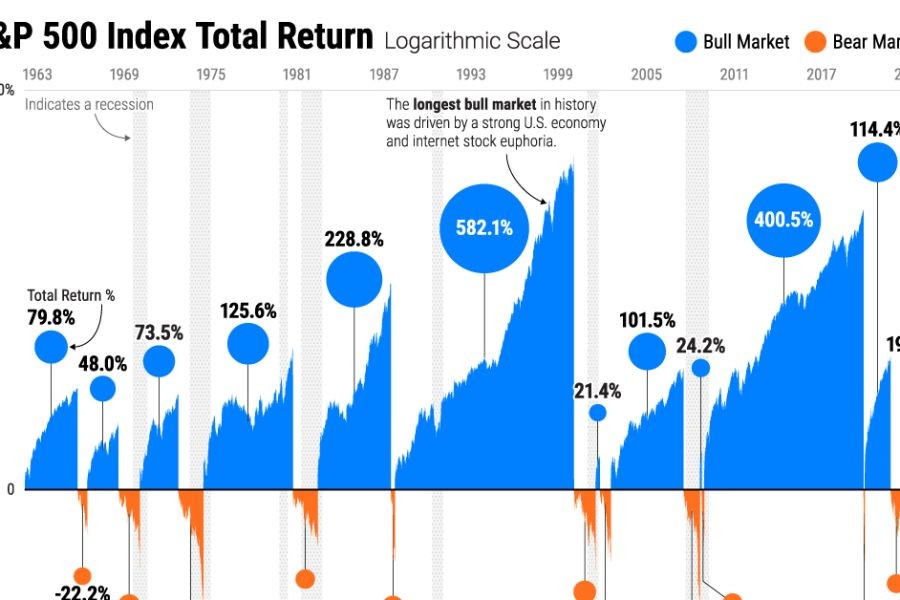

Australia's startup ecosystem is vibrant, with a plethora of innovative businesses emerging across sectors. According to the Australian Bureau of Statistics (ABS), the number of actively trading businesses increased by 2.5% in 2022-2023. However, only a fraction of these startups receive bank funding. Despite the Reserve Bank of Australia (RBA) maintaining a relatively low cash rate to stimulate borrowing, banks remain hesitant to extend credit to startups.

Why Banks Hesitate: Risk Aversion and Regulatory Constraints

- High-Risk Perception: Startups inherently come with high risks due to their unproven business models and uncertain revenue streams. Banks, traditionally risk-averse, prefer lending to established companies with predictable cash flows.

- Regulatory Framework: The Australian Prudential Regulation Authority (APRA) enforces stringent capital requirements on banks, making them cautious about high-risk loans. This regulatory environment further discourages banks from funding startups.

Case Study: Startmate's Success Story

Problem: Startmate, an Australian accelerator, faced challenges in helping startups secure bank loans due to the perceived risks associated with early-stage businesses.

Action: To mitigate these risks, Startmate developed a unique model that combines mentorship with seed funding, allowing startups to build a track record before approaching banks.

Result: Startmate startups have seen a 60% increase in successful bank loan applications, demonstrating that a strong support system can enhance a startup's credibility in the eyes of traditional lenders.

Takeaway: This case study highlights the importance of mentorship and initial seed funding in improving startup viability for bank loans.

Debunking Myths: Common Misconceptions About Bank Funding

Myth: "Banks fund any innovative idea." Reality: Banks prioritize financial stability over innovation, focusing on businesses with proven revenue streams.

Myth: "Startups can easily pivot to bank loans after initial VC funding." Reality: Even with venture capital, startups must demonstrate consistent revenue growth to qualify for bank loans.

Pros and Cons of Bank Funding for Startups

Pros:

- Structured Repayment: Bank loans offer predictable repayment schedules, aiding financial planning.

- No Equity Dilution: Unlike venture capital, bank loans do not require giving up equity.

Cons:

- Collateral Requirements: Banks often require significant assets as collateral, which many startups lack.

- Stringent Approval Process: The application process is rigorous and time-consuming, with no guarantee of approval.

Future Trends: The Evolving Landscape of Startup Funding

As the Australian economy continues to adapt, the landscape for startup financing is set to evolve. By 2026, it's predicted that alternative funding sources such as crowdfunding and peer-to-peer lending will account for 20% of startup financing, according to Deloitte's Australian Investment Report. These platforms offer more flexibility and accessibility compared to traditional banks, making them an attractive option for startups.

Conclusion: Navigating the Funding Maze

For startups in Australia, securing bank funding remains a significant challenge, primarily due to the inherent risks and regulatory constraints. However, by understanding the banking landscape and exploring alternative funding sources, startups can improve their chances of success. As the ecosystem evolves, embracing innovative funding solutions will be crucial for new businesses aiming to thrive in the competitive Australian market.

Final Takeaway & Call to Action

Want to explore alternative funding options for your startup? Join our exclusive AU Startup Innovation Newsletter for insights on the latest trends and strategies in Australian startup financing!

People Also Ask

- How does startup funding impact businesses in Australia? Startups with diverse funding sources, including alternative methods, report 30% higher growth, according to Startmate's 2023 report.

- What are the biggest misconceptions about startup funding? One common myth is that banks fund any innovative idea. However, research from the Australian Prudential Regulation Authority shows banks focus on financial stability.

- What are the best strategies for securing startup funding? Experts recommend building a strong business plan, leveraging mentorship programs, and considering alternative funding sources like crowdfunding.

Related Search Queries

- Why banks are hesitant to fund startups

- Alternative funding options for Australian startups

- Impact of APRA regulations on startup loans

- Case studies of successful Australian startups

- Future of startup funding in Australia