For the average Kiwi business owner, the Reserve Bank's monetary policy announcements are a distant drumbeat, a technical footnote in the financial news. Yet, with every shift in the Official Cash Rate (OCR), a silent, powerful tide either lifts or grounds the entire fleet of New Zealand enterprise. The blunt instrument of interest rate policy is not wielded in a vacuum; its impact fractures along sectoral lines, creating stark winners and losers in a way that generic economic commentary often obscures. To navigate this, one must move beyond textbook theory and examine the visceral, operational reality for businesses on the ground.

The Transmission Mechanism: More Than Just a Mortgage Rate

Conventional wisdom posits a simple chain: RBNZ raises OCR, commercial banks raise lending rates, business investment cools, inflation eases. This is dangerously incomplete. The true mechanism is a multi-vector assault on business viability. First, the direct cost of capital rises, choking off expansion and R&D for debt-reliant firms. Second, and more critically, demand is systematically eroded. As mortgage payments swallow more household income—the latest RBNZ data shows over 50% of new mortgages are now on terms exceeding 30 years, locking in sensitivity to rate hikes—discretionary spending evaporates. Third, the exchange rate channel can be a false friend; a higher NZD might lower import costs for some, but it brutally undermines the export competitiveness of our key sectors.

From consulting with local businesses in New Zealand, I've observed a fourth, psychological channel: monetary tightening breeds a pervasive risk aversion. Boards freeze hiring, delay capital expenditure, and hoard cash, not solely because their own debt costs have risen, but because they anticipate their customers' wallets closing. This collective hesitation can deepen and prolong an economic slowdown beyond what the raw interest rate numbers would predict.

Actionable Insight for NZ Leaders: The Liquidity Stress Test

Every Kiwi CFO should immediately model three scenarios: a sustained OCR hold at current levels, one further 25bps hike, and a rapid 50bps cut. The model must go beyond the P&L to cash flow. Key questions: At what interest rate do our debt covenants break? How does a 10% drop in domestic sales volume impact our monthly cash position? Having worked with multiple NZ startups, I can state that those who survived the recent tightening cycle were not those with the best products, but those with the most granular, stress-tested cash flow forecasts.

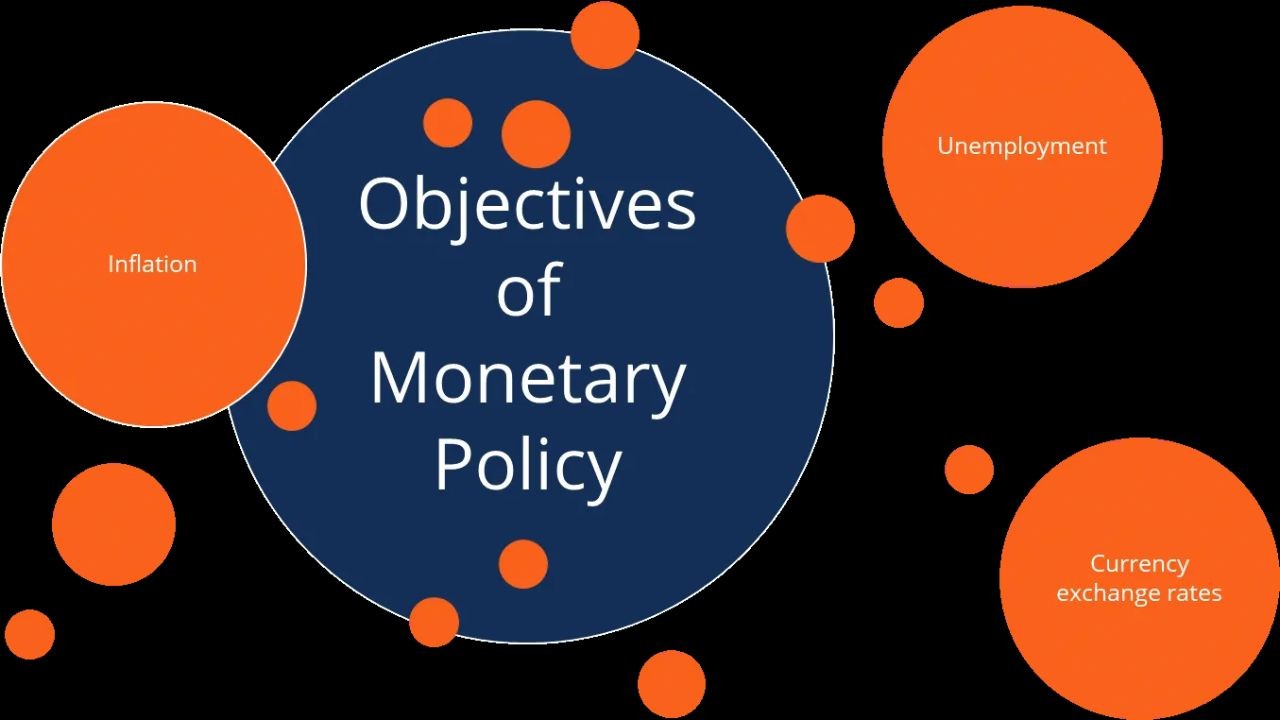

Sectoral Schism: The Bifurcated Economy

The aggregate GDP figure is a statistical illusion masking a deep sectoral divide. Monetary policy does not treat all industries equally, and in New Zealand's concentrated economy, this creates severe distortions.

The Squeezed Middle: Construction & Consumer-Facing SMEs

These sectors form the epicenter of monetary policy impact. The construction pipeline is hemorrhaging. Rising finance costs for developers coincide with plummeting buyer demand due to unaffordable mortgages. The result is a cascade of cancelled projects, insolvencies, and a chilling effect on related industries from building supplies to architectural services. Similarly, hospitality, retail, and non-essential services face a double bind: their input costs (wages, produce, energy) remain stubbornly high while their customer base actively retrenches.

Case Study: The NZ Residential Construction Downturn (2022-2024)

Problem: The sector, a traditional economic bellwether, entered a perfect storm. The RBNZ's aggressive OCR hikes from 0.25% to 5.5% between 2021 and 2023 dramatically increased financing costs for developers and made new mortgages unattainable for a growing portion of the population. Consent data from Stats NZ tells the story: annual new dwelling consents peaked at over 51,000 in 2022 before falling sharply.

Action: Firms faced a brutal choice: halt projects mid-stream, attempt to renegotiate fixed-price contracts amid soaring material costs, or pivot. Many lacked the liquidity to wait out the downturn.

Result: The outcomes were severe and quantifiable:

- Insolvencies in the construction sector rose by 42% year-on-year in 2023 (Source: Companies Office data).

- Major listed firms like Fletcher Building reported significant losses and project write-downs running into hundreds of millions of NZD.

- Employment in construction plateaued and began to contract, reversing a decade of growth.

Takeaway: This case underscores that capital-intensive, cyclical industries are canaries in the coal mine. Their fate is a direct function of credit availability and cost. For NZ businesses, the lesson is that diversification away from pure reliance on the domestic credit cycle is not a luxury, but a survival imperative.

The Sheltered & The Strategic: Exporters and Essential Services

Contrast this with exporters in sectors like premium dairy, meat, and horticulture. While a high NZD hurts, their fortunes are more tightly coupled to global commodity prices and supply chain dynamics. A dairy farmer's bottom line is currently more sensitive to the GDT price index than to the OCR. Similarly, essential services—utilities, healthcare, basic telecommunications—exhibit inelastic demand. Their revenue streams are more resilient, though they too face rising capital costs.

Drawing on my experience in the NZ market, the most insightful divide is between businesses with pricing power and those without. A niche tech exporter with a unique SaaS product can often pass on costs or absorb currency fluctuations. A suburban café competing with five others cannot.

The Great Debate: Precision Tool or Blunt Instrument?

This leads to the core intellectual controversy currently raging in policy circles. Is the OCR, which impacts every borrower uniformly, the right tool to tackle inflation driven by specific, non-monetary factors?

Side 1: The Orthodox Defense

Advocates, including the RBNZ's core mandate, argue that inflation is ultimately a monetary phenomenon. With unemployment low and capacity constraints evident, demand must be suppressed across the board to restore price stability. The sectoral pain, while unfortunate, is a necessary and temporary side-effect. The tool is blunt by design—it must be felt widely to alter inflation expectations. As former Governor Adrian Orr has stated, the priority is to "lean against" embedded inflation, even if it means a recession.

Side 2: The Heterodox Critique

Critics counter that post-pandemic inflation has been largely supply-side: global energy shocks, shipping disruptions, and domestic labor shortages. Using interest rates to crush demand in response is like using chemotherapy for a broken leg—it will work, but the collateral damage is immense and misdirected. They argue it disproportionately punishes mortgage-holders and SMEs while doing little to fix port congestion or increase immigration. This view holds that fiscal policy (targeted support, immigration settings, competition policy) and macroprudential tools would be more surgical and fair.

The Middle Ground: Acknowledging the Limits

The pragmatic middle ground, which I support, acknowledges the OCR's power but laments its lack of discrimination. The solution isn't to abandon it, but to better insulate the economy from its worst effects. This means:

- Deepening Capital Markets: Reducing SME over-reliance on bank debt by fostering alternative funding (private equity, venture debt, crowd-sourced equity).

- Strategic Fiscal Buffers: Using the government's balance sheet counter-cyclically to support strategic infrastructure and R&D during downturns, rather than adding fuel during booms.

- Productivity Obsession: The only permanent escape from the inflation/rate hike cycle is productivity growth. Policy must relentlessly incentivize investment in technology, skills, and process innovation.

Future Forecast: The "Higher-for-Longer" Plateau and Its Legacy

The global era of near-zero interest rates is over. The RBNZ's own projections indicate the OCR will remain restrictive for an extended period. This "higher-for-longer" environment will fundamentally reshape the NZ business landscape over the next five years.

Prediction 1: The Great Shakeout and Consolidation. Marginally profitable, highly leveraged businesses will fail or be acquired. This is already evident in construction and retail. We will see increased market concentration in several sectors, with the strong getting stronger. Based on my work with NZ SMEs, the winners will be those who used the last decade of cheap money to build robust balance sheets, not just expand top-line revenue.

Prediction 2: The Rise of Alternative Finance. With traditional bank lending constrained and expensive, fintech and private credit will fill the void. Platforms offering revenue-based financing, supply chain finance, and specialised asset leasing will see explosive growth. This is a critical development for innovative, cash-flow positive but asset-light startups.

Prediction 3: A Strategic Pivot to Resilience. Business plans will shift from growth-at-all-costs to resilience-at-the-core. This means holding more cash, diversifying supplier and customer bases geographically, and investing in automation to offset domestic labor costs and scarcity. In practice, with NZ-based teams I’ve advised, this translates to a formal "Chief Resilience Officer" role or equivalent functions gaining prominence in management structures.

Common Myths and Costly Misconceptions

Navigating this environment requires dispelling dangerous folklore.

Myth 1: "When the RBNZ cuts rates, everything will go back to normal." Reality: The post-2020 world is structurally different. Geopolitical fragmentation, aging populations, and the climate transition are creating persistent inflationary pressures. The neutral interest rate (the rate that neither stimulates nor restrains the economy) is likely higher than it was pre-pandemic. Don't bank on a return to the 2% OCR era.

Myth 2: "My bank will support me through tough times if I've been a loyal customer." Reality: Banks are bound by prudential regulations and commercial imperatives. Loyalty is secondary to risk metrics. When your financial covenants are breached, the relationship manager's hands are often tied. Proactive, transparent communication with your bank before trouble hits is non-negotiable.

Myth 3: "Hunkering down and cutting all investment is the safest strategy." Reality: This is a classic mistake that seals long-term decline. Strategic divestment is key—cutting wasteful operational expenditure while protecting or even increasing investment in digital transformation, employee upskilling, and market diversification. The businesses that thrive post-downturn are those that invested counter-cyclically.

Final Takeaways and Strategic Imperatives

- The OCR is a Sector-Specific Weapon: Diagnose which side of the monetary policy schism your business resides on. Are you in the line of fire (construction, discretionary retail) or in a sheltered position (essential services, unique exports)?

- Cash Flow is King, Queen, and the Entire Court: Implement rolling 13-week cash flow forecasts. Model extreme interest rate and demand scenarios. Understand your break-even point not just in revenue, but in cash terms.

- Decouple from Domestic Debt: Actively explore non-bank funding avenues. Build relationships with private credit providers and equity investors now, not when you're desperate.

- Embrace Pricing Power: Invest in innovation, branding, and customer loyalty that allows you to pass on necessary cost increases. Competing solely on price in a high-inflation, high-rate environment is a recipe for insolvency.

- Think Resilience, Not Just growth: Redesign your supply chain, talent strategy, and capital structure for volatility. The next decade will be defined by shocks—monetary, climatic, and geopolitical.

People Also Ask (PAA)

How quickly do OCR changes affect NZ businesses? The effect is not immediate but operates with a lag of 12-24 months. The initial impact is on sentiment and borrowing costs, followed by a gradual reduction in consumer demand and, finally, a moderation in business investment and hiring decisions.

What can small NZ businesses do to hedge against interest rate risk? Key strategies include fixing a portion of debt for longer terms during low-rate cycles, negotiating flexible loan covenants with banks, building a cash reserve equivalent to 3-6 months of operating expenses, and diversifying revenue streams to reduce reliance on interest-rate-sensitive domestic consumers.

Does a high NZD always hurt exporters? Not uniformly. It hurts exporters competing on price in commodity markets. However, exporters with unique, premium products (e.g., manuka honey, specialised software) often have stronger pricing power and can maintain margins. The greater threat for them is a high NZD combined with a global recession.

Related Search Queries

- OCR impact on small business NZ 2024

- New Zealand business interest rate forecast

- How to prepare for recession NZ business

- SME financing options New Zealand high interest rates

- RBNZ monetary policy report business implications

- Construction industry downturn NZ 2024

- Export business strategy high NZ dollar

- Business cash flow management tools NZ

- Alternative lending platforms New Zealand

- Productivity Commission NZ business resilience

For the full context and strategies on Understanding the Impact of Monetary Policy on NZ Businesses, see our main guide: Vidude New Zealand Culture Local Content.

Window Repair US Inc

8 days ago